Cement sales lost momentum, with decline clinker export foreseen in 2019

By Tay Lan

July 08, 2019 | 03:05 PM GMT+7

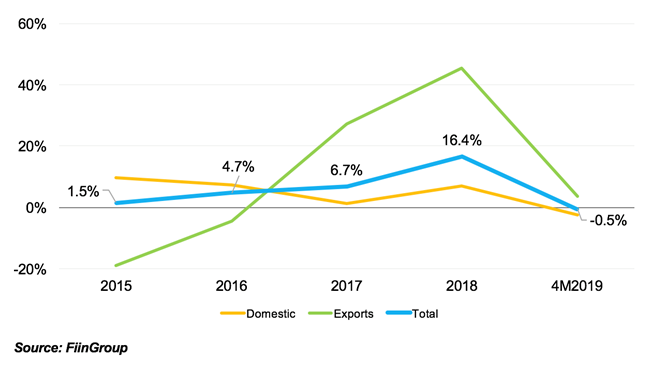

Clinker and cement sales fell 0.5 per cent in the first four months through April as a result of slowdown in domestic market and exports.

Clinker and cement sales growth, year on year.

According to FiinGroup’s market research report entitled ‘Vietnam Cement Market 2019’, the first four months of 2019 witnessed a slower cement sales growth. Domestic sales were down 2.5 per cent to 20.4 million tonnes while exports down by 3.7 per cent to reach 10.3 million tonnes for the period.

Average export price remained high with clinker free-on-board (FOB) price of $39.4 per tonne at Cam Pha port as of April 2019. Given the decreasing clinker demand from China, FiinGroup foresees a decline in clinker export volume and average price in the next quarters of the year.

Total clinker and cement sales volume reached a record high in 2018 at 93.5 million tonnes, a growth of 16.4 per cent on-year, driven by robust exports. Cement and clinker export volume recorded a year-on-year surge by 45.5 per cent to reach 28.6 million tonnes in 2018, which could be explained by rising demand from Chinese traders.

Since 2017, the Chinese government has implemented an unprecedented pollution crackdown by shutting down steel and cement factories in the effort to address China’s severe pollution, affecting 10 per cent cement production capacity in the country. Despite supply surplus on national scale, there is a certain temporary shortage in some border provinces near Vietnam.

The clinker price in the coastal regions is $66 per tonne, compared to the average export price of $38.8 per tonne in Vietnam. The high price has stimulated the traders to increase import clinker from Vietnam to meet the demand in the China coastal regions.

Meanwhile, Vietnam cement and clinker market improved significantly with solid growth of 7 per cent in 2018. The market was supported by the improved real estate market (including residential, industrial and hospitality real estate) and optimistic construction market.

Local private manufacturers have been aggressively developing new cement facilities while foreign-owned players are strengthening their position after merger and acquisition (M&A) activities.

According to FiinGroup’s database, designed capacity of Vietnam cement industry is expected to surge thanks to the aggressive expansion of local private players including Thanh Thang, Vissai, ThaiGroup (previously Xuan Thanh) and Long Son. The new facilities are located in the central region where demand is relatively low compared to the north and the south. These players specifically target export markets.

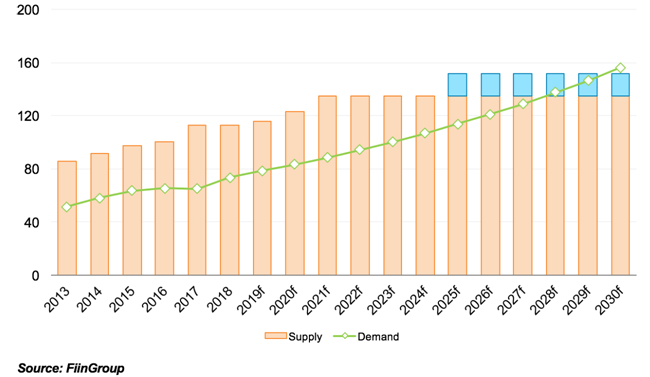

Projected cement demand and supply in Vietnam, million tonnes

Meanwhile, foreign investors are strengthening their position with sales campaign and new products. For instance, in May 2019, Siam Cement Group (SCG) has recently launched its SCG Super Cement brand to customers in central Vietnam.

Based on FiinGroup’s analysis of macroeconomics and historical cement demand from 2000, demand growth for cement is projected at a growth rate of 5 per cent until 2030. Vietnam is expected to face with continuous supply surplus before reaching the equilibrium in 2028. Even though Vietnam cement still moves in tandem with real estate boom and bust, this industry is expected to enjoy healthy growth in years to come.

As Vietnam sets its sights on becoming a high-income country by 2045, Resolution 68 lays a crucial foundation. But turning vision into reality requires not only good policy - but also unwavering execution, mutual trust and national unity.

Vietnam plans to upgrade Gia Binh Airport in Bac Ninh province into a dual-use international airport to support both military and civilian operations, the government said on Friday.

Under unforgiving conditions, the outdoor workers - the backbone of urban economies - endure the harshest impacts of climate change while remaining overlooked by social safety nets. Their resilience and struggles highlight the urgent need for better protection in the face of rising temperatures and precarious livelihoods.

Doan Van Binh, Chairman of CEO Group and Vice President of the Vietnam National Real Estate Association, introduced his latest book, “Vietnam Real Estate for Foreigners,” at a launch event in Hanoi on Friday.

Acting for increased women’s participation and leadership in climate action, Vietnam can accelerate a transition that is more inclusive, just, and impactful.

The "Steam for girls 2024" competition provides a creative platform for Steam and an opportunity for students to connect with peers from various regions within Vietnam and internationally.

![[Hỏi đáp] Bỏ thuế khoán: Hộ kinh doanh có được xuất hóa đơn đỏ không?](https://t.ex-cdn.com/theleader.vn/320w/files/news/2025/12/05/hoa-don-gtgt-1440.jpg)

![[Hỏi đáp] Bỏ thuế khoán 2026: Ngành thuế hỗ trợ hộ kinh doanh chuyển đổi thế nào?](https://t.ex-cdn.com/theleader.vn/192w/files/news/2025/12/05/z7261608772972_6406130837e396a31e34fb0dd16e0873-2230.jpg)