Auto market remains 55 per cent capacity to await Vingroup

By Minh An

September 07, 2017 | 07:11 AM GMT+7

Although some investors might concern and even question the prospect of the Vietnamese auto market, Vingroup decided to start a US$3.5 billion automobile assembly.

Vietnam Motorshow 2017. Photo: Zing.vn

The phrase "small market" is repeated four times in a four-page report by The Automotive Working Group in Vietnam Business Forum 2017 as referring to the country's auto market.

Last year, the market grew 24% with the sales of 304,000 vehicles, according to a report by the Vietnam Automobile Manufacturers Association (VAMA). And according to the The ASEAN Automotive Federation (AAF), Vietnam market's size reached 270 thousand vehicles, much lower than that of Thailand, Indonesia and Malaysia,

of which Vietnam produced and assembled about 230 thousand. Vietnam's output is equivalent to only 11% of that of Thailand and only higher than that of the Philippines.

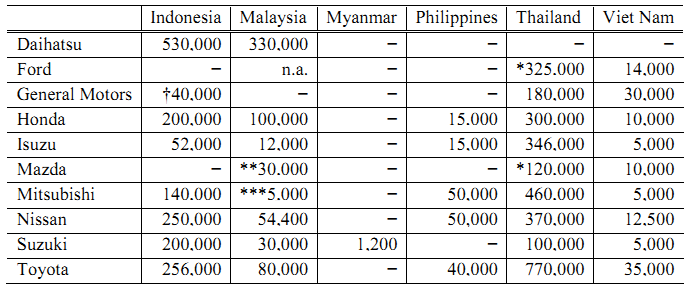

The report by the working group reveals that Vietnam's production only accounts for about 45% of the plants' capacity in the sector, with an estimated 500,000 vehicles per year. This figure is lower than Toyota's capacity itself in Thailand (770,000 units) or Daihatsu in Indonesia (530,000 units), according to JAMA.

Production capacity of some companies in ASEAN countries. Source: JAMA and Martin Schroder Research, May 2017.

Because the demand is too small, most global automotive component suppliers do not enter the market as they can not invest without being guaranteed that the original equipment manufacturer (OEMs) will maintain as well as increase production.

It is estimated that there are about 425 automotive component suppliers in Vietnam, according to Martin Schroder's automotive industry research in May 2017. These enterprises mainly come from Japan (181), Taiwan (65) and South Korea (20).

Due to the high quality standard, cost and delivery, very few domestic suppliers can meet the requirement of joining the global supply chain.

The group also said that joining the component supply market is not easy due to high standards of safety and quality.

Due to the disadvantages of the production scale, and the majority of components and materials for the production of automobiles are imported, adding more costs for domestic producers such as packaging, logistics and import taxes.

That is the reason why the cost of producing cars in Vietnam is usually higher than that in Thailand or Indonesia. The gap in production costs can range up to 10-20%, which reduces the competitiveness of domestic assembled vehicles compared to ASEAN's completelt built units (CBU) from 2018, when the preferential tariff for CBU from ASEAN countries will be cut to 0%.

The working group indicates that in order to solve the above problems, there must be sufficient production output for both vehicles and components. However, the market has to be large enough to achieve the economies of scale for both vehicles assembled domestically and automobile auxiliary industries to improve cost efficiency.

As Vietnam sets its sights on becoming a high-income country by 2045, Resolution 68 lays a crucial foundation. But turning vision into reality requires not only good policy - but also unwavering execution, mutual trust and national unity.

Vietnam plans to upgrade Gia Binh Airport in Bac Ninh province into a dual-use international airport to support both military and civilian operations, the government said on Friday.

Under unforgiving conditions, the outdoor workers - the backbone of urban economies - endure the harshest impacts of climate change while remaining overlooked by social safety nets. Their resilience and struggles highlight the urgent need for better protection in the face of rising temperatures and precarious livelihoods.

Doan Van Binh, Chairman of CEO Group and Vice President of the Vietnam National Real Estate Association, introduced his latest book, “Vietnam Real Estate for Foreigners,” at a launch event in Hanoi on Friday.

Acting for increased women’s participation and leadership in climate action, Vietnam can accelerate a transition that is more inclusive, just, and impactful.

The "Steam for girls 2024" competition provides a creative platform for Steam and an opportunity for students to connect with peers from various regions within Vietnam and internationally.